Storage units insurance coverage

What is storage unit insurance and why is it important?

Storage unit insurance is a type of insurance that financially covers personal possessions stored in a storage unit. It protects against problems like theft, vandalism, and weather damage. Storage units are exposed to risks that can damage or destroy belongings, making storage unit insurance a necessary financial safety net if things go wrong.

It is important to note that some storage facilities require renters to have insurance as part of the rental agreement. This ensures that both the renter and the facility are protected from potential liabilities, so it is important to double-check the terms of the agreement or ask a manager at the storage facility about insurance requirements.

Types of coverage available for storage unit contents

Similar to other types of insurance, storage unit insurance involves paying a low monthly or annual premium in exchange for coverage that can secure thousands of dollars worth of protection for belongings. Depending on the policy, the following types of coverage may be available:

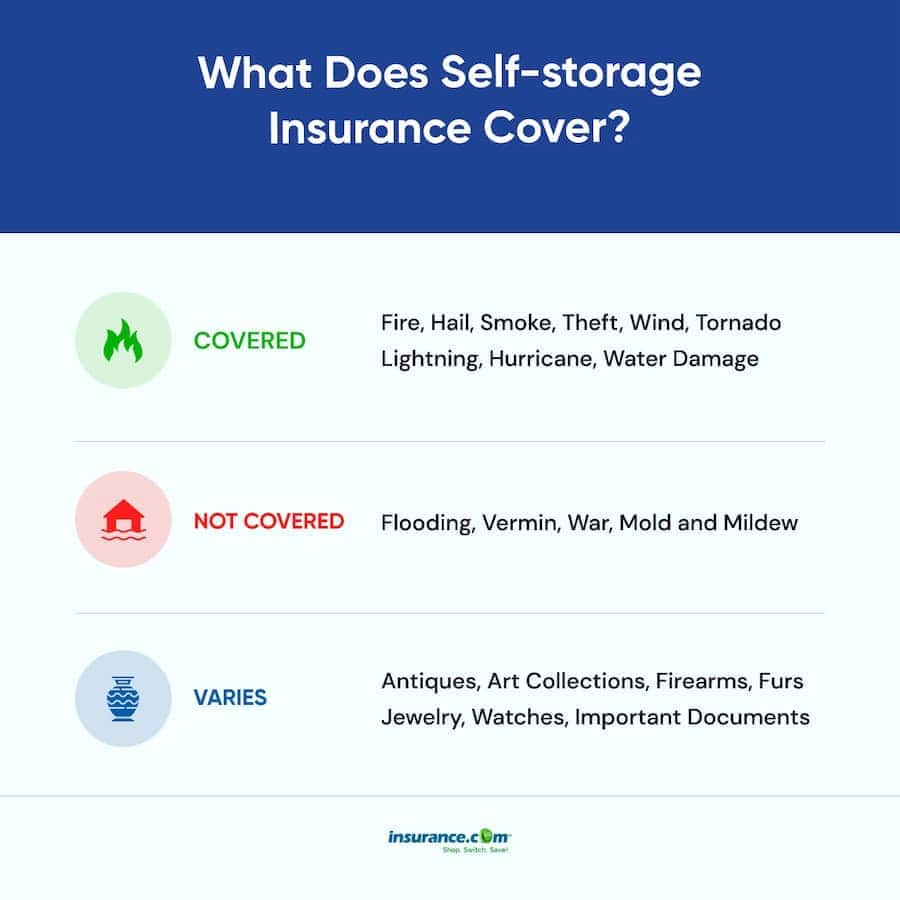

Named perils coverage: This type of policy covers specific risks that are explicitly listed in the policy, such as theft, fire, or water damage.

All-risk coverage: This type of policy covers damage or loss resulting from any cause not specifically excluded in the policy. It is typically more expensive than named perils coverage.

Full-value coverage: This coverage option ensures that the full value of all belongings in the storage unit is covered in the event of total loss or destruction, regardless of the value of individual items.

It is important to carefully consider the coverage options available and choose a policy that adequately protects stored items from potential damage or loss.

While storage unit insurance cannot cover every instance of damage or loss, it provides a valuable safety net for personal possessions stored in a storage unit. Investing in storage unit insurance can provide peace of mind and financial protection in case of unforeseen circumstances.

Homeowners Insurance Coverage for Storage Units

When looking to store personal belongings outside of the home, it’s important to consider insurance coverage for potential losses or damages. While many storage facilities require some form of insurance for tenants, homeowners insurance policies may also provide coverage for the contents of a storage unit.

How off-premises personal property coverage in homeowners policies can provide insurance for storage unit contents

Most homeowners insurance policies include coverage for personal property even when it’s not inside the home. Known as off-premises coverage, this can extend to items stored in a commercial storage unit. However, it’s important to note that the coverage limits for off-premises belongings may be less than the limits for items inside the home.

For example, if the policy has a limit of $100,000 for personal belongings inside the home, the off-premises coverage limit may only be $10,000. This means that if the storage unit contains items worth more than $10,000, the homeowner may not have enough coverage to replace everything if it is lost or damaged.

Covered perils included in typical off-premises coverage

Off-premises coverage typically includes protection against the same perils as personal property insurance inside the home. This can include:

– Fire or lightning

– Windstorm or hail

– Theft or vandalism

– Damage from vehicles or aircraft

– Explosion

– Smoke

– Falling objects

– Weight of ice or snow

It’s important to review the specific policy language to understand what is and is not covered for off-premises personal property.

While off-premises coverage can offer some level of protection for storage unit contents, it’s important to consider the value of the items being stored and whether additional insurance is necessary. Some storage facilities may offer their own insurance policies, but these may have lower coverage limits than a homeowners policy. Consider speaking with an insurance agent to understand the best options for protecting personal belongings in storage.

Yardi Commercial Property Insurance for Storage Units

For commercial property owners and managers, offering insurance coverage for storage unit tenants can be a valuable amenity. Yardi offers the GoodShield Protection Plan, which provides reliable protection for stored belongings and easy online enrollment for tenants. However, some facilities may prefer to offer their own commercial property insurance policies. Here are some benefits and considerations of Yardi’s commercial property insurance for storage units.

Benefits and cost savings of Yardi Commercial Property insurance for storage units

One advantage of using Yardi’s insurance program is the cost savings. GoodShield guarantees monthly costs without increases resulting from past claim activity. Additionally, program charges and tracking are built right into the Yardi property management platform, with automated reporting to minimize charge reconciliation work.

For tenants, the ease of online enrollment is a key benefit. GoodShield’s pre-approval for protection makes signing up fast and easy. Tenants are conveniently billed for GoodShield with their monthly storage unit rent, so they don’t have to worry about separate insurance payments or invoices.

Coverage provided by Yardi and maximum limits

GoodShield provides coverage for stored belongings against perils such as fire, theft, and water damage. The maximum coverage limit per occurrence is $5,000, with a $100 deductible. The program is available in most states, with some exceptions and limitations. It’s important to review the coverage details and limitations carefully before choosing an insurance program for storage units.

While Yardi’s GoodShield program offers benefits such as cost savings and convenience for tenants, it’s important to carefully consider the specific needs and circumstances of your storage facility. Some facilities may prefer to offer their own commercial property insurance policies, with higher coverage limits or additional optional coverage, such as flood or earthquake insurance. Consider speaking with an insurance agent to understand the best options for your storage facility and tenants.

Additional Coverage Options for Storage Units

When storing personal belongings in a storage unit, it’s important to ensure that there is adequate insurance coverage for potential losses or damages. While off-premises coverage in homeowners insurance policies may offer some protection, it may not be enough for certain valuable items or in the event of a total loss. In such cases, additional coverage options may be necessary.

When and why you may need additional coverage for storage unit contents

There are several scenarios where additional coverage beyond off-premises coverage may be necessary. These include:

– High-value items: If the storage unit contains items worth more than the off-premises coverage limit of the homeowners policy, additional insurance may be necessary to fully protect these items.

– Specialized items: Certain items, such as antiques, artwork, or collectibles, may require specialized coverage beyond standard off-premises coverage.

– Total loss: In the event of a total loss, such as a fire or natural disaster, the coverage limit of the homeowners policy may not be enough to fully replace all of the stored items.

In these situations, additional coverage options can provide a higher level of protection and peace of mind.

Costs and options for increasing coverage beyond off-premises coverage

There are several options for increasing coverage beyond off-premises coverage, each with its own cost and benefits. These include:

– Endorsements: An endorsement is a policy add-on that increases coverage for specific items or perils. Endorsements can be added to a homeowners policy to increase the coverage limits for off-premises personal property. This may be a cost-effective option for those with only a few high-value items that require additional coverage.

– Standalone policies: A standalone storage unit insurance policy can provide comprehensive coverage for all items stored in the unit. These policies may offer higher coverage limits and broader coverage than a homeowners policy endorsement. However, they can also be more expensive.

– Storage facility insurance: Some storage facilities offer their own insurance policies for tenants. While these policies may be convenient, they may have lower coverage limits or exclusions than a homeowners policy endorsement or standalone policy.

It’s important to evaluate the costs and benefits of each option to determine the best fit for individual needs and budgets. Speaking with an insurance agent can also provide additional guidance and clarity on coverage options.

Therefore, while off-premises coverage in homeowners insurance policies may provide some protection for storage unit contents, additional coverage may be necessary depending on the value and type of items being stored. Understanding the available options and working with an insurance agent can help ensure that personal belongings in storage are fully protected.

Renters Insurance Coverage for Storage Units

How renters insurance can provide coverage for belongings in a storage unit

Renters insurance policies generally provide coverage for personal property both on and off-premises, meaning that items stored in a self-storage unit can be covered. The coverage is against the same perils as it would be at home, including fire, theft, vandalism, and certain types of water damage. However, coverage for personal property in storage is limited by the policy’s sub-limit.

Limitations and exclusions to coverage provided by renters insurance policies

The coverage limit for items in a storage unit is typically a percentage of the policy’s personal property coverage limit. The exact sub-limit depends on the policy and the insured’s location, but it is usually around 10% of the personal property limit. If the total value of the stored items exceeds this limit, renters may need to purchase additional coverage to ensure full protection.

Additionally, renters insurance policies may have exclusions for certain types of items, such as jewelry or electronics. A policy may also have limitations on coverage for certain perils, like floods or earthquakes. It’s important to carefully review the policy’s terms and conditions to understand what is and isn’t covered.

Additional Coverage Options for Storage Units

When off-premises coverage in a renters insurance policy isn’t enough to cover stored items or specific types of items, additional coverage options may be necessary.

When and why you may need additional coverage for storage unit contents

Additional coverage may be necessary for high-value items, specialized items, or in the event of a total loss due to fire or natural disaster. Renters may consider additional coverage when the value of the items being stored exceeds the sub-limit set by their policy.

Costs and options for increasing coverage beyond off-premises coverage

There are a few options to increase coverage for stored items beyond what is offered by renters insurance policies. These include adding an endorsement to the renters policy to increase coverage limits for off-premises personal property, purchasing a standalone storage unit insurance policy, or utilizing insurance policies offered by the storage facility.

Endorsements can be a cost-effective option for those with only a few high-value items that require additional coverage. Standalone policies may offer higher coverage limits and broader coverage than a homeowners policy endorsement, but they can also be more expensive. The coverage limits and exclusions of any insurance policy offered by a storage facility should be carefully reviewed.

Therefore, renters insurance policies generally provide coverage for personal property stored in a self-storage unit, but the coverage is subject to a sub-limit. Additional coverage options may be necessary when storing high-value or specialized items, or in the event of a total loss. Renters should review their policy’s terms and conditions and consider additional coverage options to ensure proper protection of personal property stored off-premises.

Variances in Coverage by Storage Companies

Storage unit companies offer insurance coverage for personal belongings stored on their premises. It’s important to understand the coverage provided by each storage company as it can vary.

The differences in coverage provided by various storage unit companies

Most storage unit companies offer reimbursement based on the square footage of the unit in the event of a loss or damage. However, the coverage limits can vary by company. It’s important to review the policy terms and conditions to understand the maximum reimbursement amount for personal belongings.

In addition to coverage limits, the financial protection provided can also differ. For instance, some storage companies may offer “actual cash value” policies that factor in depreciation when reimbursing customers for losses or damages. Others may provide a “replacement cost basis” policy which would cover the full cost of replacing the item lost or damaged.

Factors to consider when choosing a storage company for insurance purposes

When selecting a storage company for insurance purposes, there are several factors to consider:

– Security: Look for a storage company that has measures in place to ensure the safety and security of personal belongings. This includes security cameras, security personnel, and secure access protocols.

– Coverage Limits: Review the storage company’s policy beforehand to understand the maximum reimbursement amount for personal belongings.

– Financial Protection: Inquire about the type of financial protection offered by the storage company. It’s important to understand whether the policy is provided on an actual cash value or replacement cost basis.

– Third-Party Insurers: Find out whether the storage company works with third-party insurers to offer insurance policies. If so, it’s important to research the reputation of the third-party insurer to ensure adequate protection for personal belongings.

It’s essential to properly choose a storage facility that meets individual needs and provides adequate insurance coverage. Doing thorough research and understanding the differences in coverage offered by different storage unit companies can help make an informed decision and provide peace of mind.

Cost of Storage Unit Insurance Coverage

When renting a storage unit, insurance coverage can protect personal belongings in the event of damage or loss. However, it’s important to understand the cost of coverage to determine whether it’s a necessary expense.

Factors affecting the cost of storage unit insurance coverage

Several factors can affect the cost of storage unit insurance coverage, including:

– Value of Personal Property: The higher the value of personal property being stored, the more expensive the insurance coverage may be.

– Location: Storage unit insurance can vary in cost depending on location, as areas with a higher risk of natural disasters or theft may have higher insurance premiums.

– Coverage Limit: The maximum amount of reimbursement available for personal belongings can also impact the cost of insurance coverage.

– Deductible: Insurance policies typically have a deductible, which is the amount the policyholder is responsible for paying before the insurance company covers any losses or damages. A higher deductible can result in lower insurance premiums.

Typical cost ranges and how to obtain affordable coverage options

The cost of storage unit insurance coverage can range from 50 cents to $2 for every $100 value amount of storage, with deductibles ranging from $100 to $500. However, it’s always wise to check with the storage facility to determine the cost of their insurance coverage and review their policy terms and conditions.

To obtain affordable coverage options, policyholders can consider:

– Bundling: Some insurance companies offer discounts for combining storage unit insurance coverage with other policies, such as home or auto insurance.

– Shopping around: It’s important to compare insurance coverage options from different providers to ensure the most coverage for the best price.

– Increasing the deductible: A higher deductible can lower insurance premiums, but policyholders should ensure they can afford to pay the deductible in the event of a loss or damage.

Therefore, the cost of storage unit insurance coverage can vary depending on several factors, such as personal property value, location, coverage limit, and deductible. To obtain affordable coverage options, policyholders can bundle policies, shop around for different providers, or increase their deductible. Understanding the cost of coverage can help determine whether it’s a necessary expense and ensure adequate financial protection for personal belongings in storage.

Filing a Claim for Storage Unit Insurance Coverage

Steps to take in the event of damage or loss to items stored in a unit

Unfortunately, accidents can happen when personal belongings are stored in a storage unit. In such an event, the first step to take is to fill out an incident report provided by the storage company. This report will help to establish the facts of the incident and provide important details for the insurance claim process. One should also take photos of the damage or loss, as well as any supporting documents that may be relevant to the incident.

Once the incident report and supporting documents have been completed, the next step is to contact the insurance provider and/or storage company. The insurance provider will require proof of ownership and value of any items that were lost or damaged. It’s essential to provide as much relevant information as possible to expedite the claims process. After the claim is filed, the insurance provider will send an adjuster to inspect the damage and provide a determination of the amount of reimbursement to be provided.

Important information to have when filing a claim with insurance providers or storage companies

Having all the necessary documentation on hand can help to expedite the claims process. It’s important to have the following information readily available when filing a claim:

– Incident report

– Supporting documents and photographs

– Proof of ownership and value of items lost or damaged

– Contact information for the storage company and insurance provider

It’s important to note that timing is also critical when filing a claim. The incident should be reported to the storage company and insurance provider as soon as practical, as there may be time limits involved in the claims process. Failure to report the incident in a timely manner may result in a denial of the claim.

Therefore, it’s essential to understand the coverage provided by storage unit companies and select a company that meets individual needs and provides adequate insurance coverage. In the event of damage or loss to personal belongings, it’s important to gather all the necessary documentation and fill out an incident report as soon as possible. Contacting the insurance provider and/or storage company in a timely manner with all the necessary information can help expedite the claims process and provide peace of mind.

Conclusion and Frequently Asked Questions

Summary of key points regarding storage unit insurance coverage

So, self-storage insurance coverage is an important consideration for individuals and businesses that store personal belongings in storage units. While some homeowners or renters insurance policies may provide coverage for items stored in a storage unit, stand-alone storage unit insurance policies may offer more comprehensive coverage. It’s important to take inventory of personal belongings and choose a storage company and insurance policy that provides adequate coverage.

In the event of damage or loss to personal belongings, it’s important to gather all necessary documentation and fill out an incident report as soon as possible. Contacting the insurance provider and/or storage company in a timely manner with all the necessary information can help expedite the claims process and provide peace of mind.

Answers to common questions about storage unit insurance coverage

Q: Do I need insurance when leasing a storage unit?

A: It depends on the policies of the storage company and the individual circumstances. Some storage companies may require insurance coverage, while others may not. Even if insurance coverage is not required, it’s important to consider the potential risks of storing personal belongings and consider obtaining adequate insurance coverage.

Q: Does homeowners or renters insurance cover items in a storage unit?

A: In some cases, homeowners or renters insurance policies may provide coverage for items stored in a storage unit. However, coverage may be limited or may not extend to all types of damage or loss. It’s important to review the details of individual insurance policies and consider obtaining stand-alone storage unit insurance for more comprehensive coverage.

Q: What should I do if personal belongings are damaged or lost in a storage unit?

A: In the event of damage or loss to personal belongings, the first step is to fill out an incident report provided by the storage company. It’s important to take photos of the damage or loss, as well as any supporting documents that may be relevant to the incident. Once the incident report and supporting documents have been completed, the next step is to contact the insurance provider and/or storage company.

Q: What information is necessary when filing a claim for storage unit insurance coverage?

A: When filing a claim for storage unit insurance coverage, it’s important to have the incident report, supporting documents and photographs, proof of ownership and value of items lost or damaged, and contact information for the storage company and insurance provider readily available. Timing is also critical, and the incident should be reported to the storage company and insurance provider as soon as practical.

Q: What coverage do stand-alone storage unit insurance policies typically provide?

A: Stand-alone storage unit insurance policies may provide coverage for a variety of types of damage or loss, including theft, fire, water damage, and damage from vermin or fungus. Policies may also provide coverage for personal liability and medical expenses in the event of an accident or injury on the storage unit property. It’s important to review individual policies and select a policy that meets individual needs and provides adequate coverage.

Check out Storage unit insurance cost.

1 thought on “Storage units insurance coverage”