**Introduction**

When it comes to storing your belongings in a storage unit, it is important to consider the insurance coverage you have for those items. Renters insurance and homeowners insurance both provide coverage for items stored in storage units, but the extent of coverage may vary depending on the insurance company and policy type. In this blog post, we will explore the coverage options for storage units under renters insurance and homeowners insurance policies.

**Overview of renters insurance coverage for storage units**

Renters insurance is designed to protect your personal belongings from various risks, including theft, fire, and water damage. In many cases, renters insurance policies do cover items stored in a storage unit. However, the coverage may be subject to certain limitations and conditions.

Here are some key points to consider regarding renters insurance coverage for storage units:

– Coverage may be limited to a certain percentage of the total personal property coverage in your policy.

– Some insurance companies may require you to specify the storage unit and its location when purchasing the policy.

– Certain high-value items, such as jewelry and artwork, may have limited coverage or require additional coverage.

To determine the specific coverage for your stored belongings, it is important to review your renters insurance policy and contact your insurance provider.

**Importance of proper insurance coverage for stored belongings**

Having insurance coverage for your stored belongings is crucial for protecting your financial investment in these items. Without proper coverage, you could potentially face significant financial loss due to theft, damage, or other unforeseen events.

Here are some reasons why having the right insurance coverage for your stored belongings is important:

– **Financial protection**: In the event of theft, fire, or other covered perils, having insurance can provide financial compensation to replace or repair your belongings.

– **Peace of mind**: Knowing that your stored items are covered can give you peace of mind and alleviate any worries about potential loss.

– **Storage company requirements**: Some storage companies may require you to have a home insurance or storage insurance policy before renting a storage unit. Having the proper insurance coverage can ensure compliance with these requirements.

– **Protection against liability**: If someone is injured or suffers property damage in relation to your stored items, your insurance coverage may provide liability protection.

It is important to review your insurance policy and understand the coverage provided for items stored in a storage unit. If you have any questions or concerns, it is recommended to speak with your insurance provider to ensure you have the appropriate coverage in place.

Therefore, both renters insurance and homeowners insurance can provide coverage for items stored in storage units, but the extent of coverage may vary. Reviewing your policy, understanding the limitations, and ensuring proper coverage is in place can help protect your stored belongings and provide peace of mind.

Understanding Renters Insurance Coverage

Explanation of how renters insurance works

Renters insurance provides coverage for your personal belongings in case of damage or theft. This includes items stored in a storage unit. The coverage for your storage unit will depend on the insurance company and the type of policy you have. It is important to review your policy and speak with your insurance agent to understand what is covered and what is not.

Overview of coverage limits and exclusions

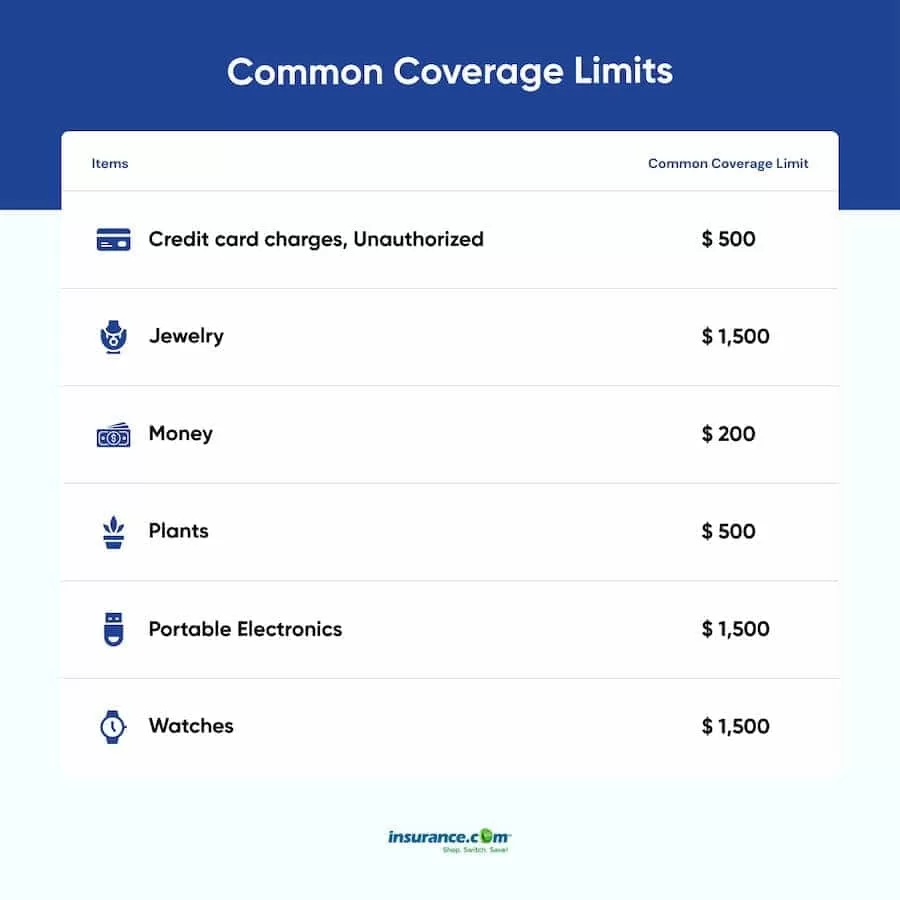

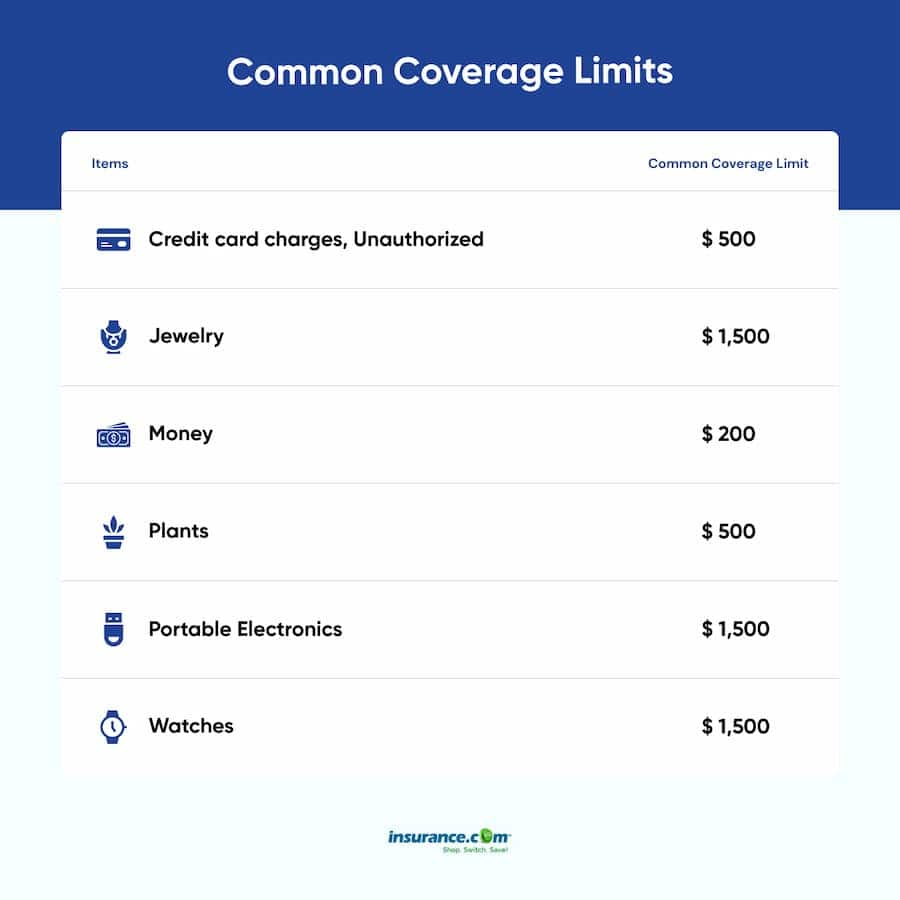

Renters insurance typically has coverage limits for certain categories of items, such as jewelry, electronics, and collectibles. Make sure to review your policy to understand these limits and consider purchasing additional coverage if needed.

Some common exclusions that may apply to storage units include:

– Damage caused by flooding or earthquakes: Renters insurance generally does not cover damage caused by natural disasters like floods or earthquakes. However, you may be able to purchase additional coverage for these events.

– Damage caused by negligence or lack of maintenance: If your items are damaged due to your own negligence or lack of maintenance, such as failing to secure the storage unit properly, your insurance may not cover the damage.

– Unauthorized access: If someone gains unauthorized access to your storage unit and steals your belongings, your renters insurance will typically cover the theft. However, if you gave someone permission to access the unit and they steal your belongings, your coverage may be limited or excluded.

It is important to read your policy carefully and understand the coverage and exclusions specific to your insurance company and policy. If you have any questions, contact your insurance agent for clarification.

Understanding Homeowners Insurance Coverage

Explanation of how homeowners insurance works

Homeowners insurance provides coverage for your home and its contents. This includes coverage for items stored in a storage unit. The off-premises personal property coverage section of your homeowners insurance policy typically includes coverage for items stored in a storage unit.

Overview of coverage limits and exclusions

Similar to renters insurance, homeowners insurance has coverage limits for certain categories of items. It is important to review your policy to understand these limits and consider purchasing additional coverage, such as a floater policy, for high-value items.

Some common exclusions that may apply to storage units under homeowners insurance include:

– Damage caused by flooding or earthquakes: Homeowners insurance usually does not cover damage caused by floods or earthquakes. Separate coverage may need to be purchased for these events.

– Unauthorized access: If someone gains unauthorized access to your storage unit and steals your belongings, your homeowners insurance should cover the theft, subject to any applicable deductibles and coverage limits.

– Negligence or lack of maintenance: If your items are damaged due to your own negligence or lack of maintenance, such as failing to secure the storage unit properly, your insurance may not cover the damage.

It is important to review the specific coverage and exclusions in your homeowners insurance policy and speak with your insurance agent if you have any questions. Additional coverage options may be available to enhance your protection for items in storage units.

Understanding Renters Insurance Coverage

Explanation of how renters insurance works

Renters insurance provides coverage for personal belongings in case of damage or theft, including items stored in a storage unit. The coverage for the storage unit will vary depending on the insurance company and policy type. It is important for renters to review their policy and consult with their insurance agent to understand what is covered.

Overview of coverage limits and exclusions

Renters insurance typically has coverage limits for certain categories of items, such as jewelry and electronics. It is important to review the policy to understand these limits and consider purchasing additional coverage if necessary.

Some common exclusions that may apply to storage units include:

– Damage caused by natural disasters: Renters insurance usually does not cover damage caused by flooding or earthquakes. Additional coverage can be purchased for these events.

– Damage caused by negligence: If the items in the storage unit are damaged due to negligence or lack of maintenance, such as not securing the unit properly, the insurance may not cover the damage.

– Unauthorized access: If someone steals belongings from the storage unit without permission, renters insurance typically covers the theft. However, if the person had permission to access the unit and steals belongings, the coverage may be limited or excluded.

It is important to carefully read the policy and understand the coverage and exclusions specific to the insurance company and policy. Any questions should be directed to the insurance agent for clarification.

Understanding Homeowners Insurance Coverage

Explanation of how homeowners insurance works

Homeowners insurance provides coverage for the home and its contents. This includes coverage for items stored in a storage unit. The off-premises personal property coverage section of the homeowners insurance policy usually includes coverage for items in a storage unit.

Overview of coverage limits and exclusions

Similar to renters insurance, homeowners insurance has coverage limits for certain categories of items. It is important to review the policy to understand these limits and consider purchasing additional coverage, such as a floater policy, for high-value items.

Some common exclusions that may apply to storage units under homeowners insurance include:

– Damage caused by natural disasters: Homeowners insurance generally does not cover damage caused by floods or earthquakes. Separate coverage may need to be purchased for these events.

– Unauthorized access: If someone steals belongings from the storage unit without permission, homeowners insurance should cover the theft, subject to any applicable deductibles and coverage limits.

– Negligence or lack of maintenance: If the items in the storage unit are damaged due to negligence or lack of maintenance, such as not securing the unit properly, the insurance may not cover the damage.

It is important to review the specific coverage and exclusions in the homeowners insurance policy and consult with the insurance agent for any questions. Additional coverage options may be available to enhance the protection for items in storage units.

State Farm Renters Insurance

Overview of State Farm as a renters insurance provider

State Farm is a well-known insurance company offering various insurance products, including renters insurance. They have a strong reputation for customer service and reliable coverage.

Benefits and features of State Farm renters insurance

– Coverage for personal belongings: State Farm renters insurance provides coverage for personal belongings in case of damage or theft, including items stored in a storage unit, subject to policy terms and conditions.

– Liability protection: State Farm renters insurance also provides liability protection, which can help cover legal expenses and damages if a guest is injured in your rented property or you accidentally damage someone else’s property.

– Additional living expenses: If your rented property becomes uninhabitable due to a covered loss, State Farm renters insurance may cover additional living expenses, such as hotel stays or temporary accommodations.

– Discounts: State Farm offers various discounts that may help lower the cost of renters insurance. These discounts may be available for factors such as having multiple policies with State Farm or installing safety features in your rented property.

Summary:

Renters insurance and homeowners insurance can provide coverage for the personal belongings stored in a storage unit, but the specific coverage and exclusions may vary depending on the insurance company and policy. It is crucial to review the policy terms and consult with the insurance agent to understand the coverage limits, exclusions, and options for additional coverage. State Farm is a reputable insurance provider that offers renters insurance with features such as coverage for personal belongings, liability protection, and discounts.

Personal Property Coverage in Storage Units

Explanation of how renters insurance extends to storage units

Renters insurance is designed to protect your personal belongings, whether they are in your apartment or in storage. While coverage for items in storage units can vary between insurance companies and policies, many renters insurance policies do provide coverage for storage units. This means that if your belongings in storage are damaged or stolen, you may be able to file a claim with your renters insurance to receive compensation.

It is important to note that the coverage for storage units typically falls under the off-premises personal property coverage section of your renters insurance policy. This coverage extends the protection of your personal property beyond the boundaries of your apartment to include items stored in a storage unit. However, it’s always recommended to review your specific policy and speak with your insurance agent to understand the exact coverage details.

Coverage limits for personal property stored in storage units

Renters insurance policies often have coverage limits for certain categories of items, such as jewelry, electronics, and collectibles. These limits specify the maximum amount of coverage you have for these types of items. If the value of your stored belongings exceeds these limits, you may want to consider purchasing additional coverage, also known as a floater policy, to ensure they are adequately protected.

Additionally, there are some common exclusions that may apply to storage units under renters insurance. For example, damage caused by flooding or earthquakes is typically not covered by standard renters insurance policies. If you live in an area prone to these types of natural disasters, you may want to consider purchasing additional coverage specifically for these events.

Similarly, if your items in storage are damaged due to your own negligence or lack of maintenance, such as failing to properly secure the storage unit, your insurance may not cover the damage. It is essential to understand the exclusions and limitations of your specific policy by carefully reading through your policy documents or reaching out to your insurance agent for clarification.

Overall, renters insurance can provide valuable coverage for your personal belongings, not only in your apartment but also in storage units. To ensure you have the right level of protection, it is crucial to review and understand your policy, know the coverage limits, and consider additional coverage if necessary. By doing so, you can have peace of mind knowing that your stored belongings are safeguarded in case of unexpected events.

Additional Limits and Protection

Information on any additional coverage limits provided by State Farm

State Farm is one of the largest insurance providers in the United States, offering a range of insurance products, including renters insurance. When it comes to coverage for items in storage units, State Farm policies may have additional limits and protection in place.

State Farm renters insurance typically extends coverage to personal property stored in a storage unit, similar to other insurance companies. However, it’s essential to review your specific policy and speak with a State Farm agent to understand the exact coverage limitations and any additional protection that may be available.

State Farm may have specific coverage limits for certain categories of items, such as jewelry, electronics, and collectibles. These limits determine the maximum amount of coverage you have for these types of belongings. If the value of your stored items exceeds these limits, you may want to consider purchasing additional coverage to ensure adequate protection.

It’s important to note that State Farm renters insurance policies may also have exclusions for certain perils or events. For example, damage caused by natural disasters like flooding or earthquakes may not be covered under the standard policy. If you live in an area prone to these types of events, it’s advisable to discuss with a State Farm agent about purchasing additional coverage specifically tailored to these perils.

Benefits of discussing storage unit coverage with an agent

While researching and reading policy documents can provide valuable information, speaking with a State Farm agent can offer additional benefits when it comes to understanding the coverage for items in storage units.

State Farm agents are insurance professionals who can provide personalized guidance and assist in customizing your policy to meet your individual needs. By discussing your storage unit coverage with an agent, you can gain a clear understanding of the specific limits and exclusions in your policy.

An agent can also help identify any gaps in coverage and recommend additional policies or enhancements to ensure your stored belongings are adequately protected. They can assess your individual situation, taking into account the value of your items and any specific risks associated with the storage facility or location.

Additionally, an agent can explain the claims process and provide guidance on how to file a claim in case of damage or theft of items in storage. They can help you understand the documentation required, the coverage limits that apply, and any deductibles or limitations that may come into play.

Overall, discussing your storage unit coverage with a State Farm agent can provide you with peace of mind and ensure you have the right level of protection for your personal belongings. Their expertise and knowledge of the insurance products offered by State Farm can help you make informed decisions and navigate the complexities of insurance coverage.

Remember, renters insurance policies and coverage for storage units can vary, so it’s essential to review your specific policy and consult with a State Farm agent to fully understand your coverage and any additional options available to you. By doing so, you can have confidence that your stored belongings are safeguarded in case of unexpected events.

Exclusions and Exceptions

Details of any items not covered by renters insurance in storage units

While renters insurance generally provides coverage for items in storage units, there are certain exceptions and exclusions to be aware of. These may vary depending on your insurance company and specific policy. Here are some common situations where your renters insurance may not cover your stored belongings:

– Damage caused by flooding or earthquakes: Standard renters insurance policies typically do not cover damage caused by natural disasters such as flooding or earthquakes. If you live in an area prone to these events, it is important to consider purchasing additional coverage specifically for these risks.

– Damage due to negligence or lack of maintenance: If your belongings in storage are damaged as a result of your own negligence or failure to properly maintain the storage unit, your insurance may not cover the damages. It is crucial to ensure that you properly secure the storage unit and take necessary precautions to avoid damage.

– Illegal activities or possession of prohibited items: Renters insurance does not cover belongings used for illegal activities or possession of prohibited items. If your stored items are involved in illegal activities or violate the terms and conditions of the storage facility, your insurance will likely not provide coverage.

Information on exclusions or restrictions related to valuable items

Renters insurance policies often have coverage limits for certain categories of valuable items, such as jewelry, electronics, and collectibles. These limits specify the maximum amount of coverage you have for these types of items. If the value of your stored valuables exceeds these limits, you may want to consider purchasing additional coverage, such as a floater policy, specifically for these valuable items.

Additionally, it’s important to note that some renters insurance policies may have restrictions or exclusions on certain types of valuables. For example, high-value items like fine art or expensive jewelry may require separate coverage or a separate policy altogether. It is recommended to review your policy documents or speak with your insurance agent to understand any specific exclusions or limitations that may apply to valuable items in storage.

Knowing the potential exceptions and restrictions can help you make informed decisions about the level of coverage you need for your stored belongings. It’s always a good idea to read your policy thoroughly and consult with your insurance agent to ensure you have the necessary coverage for your specific situation.

Therefore, renters insurance can provide coverage for your personal belongings stored in a storage unit, but it is important to understand the details of your policy and any exclusions that may apply. By reviewing your policy and considering additional coverage if necessary, you can ensure that your stored belongings are adequately protected in case of unexpected events.

Claims Process for Stored Belongings

Step-by-step guide on filing a claim for damaged or stolen items in storage

Filing a claim for damaged or stolen items in storage can be a stressful process, but understanding the steps involved can help make it easier. Here is a step-by-step guide on how to file a claim for your stored belongings:

1. Review your insurance policy: Before filing a claim, it is important to review your renters insurance policy to understand the terms and conditions of coverage for stored belongings. Pay close attention to any limitations, exclusions, or deductible amounts that may apply.

2. Document the damage or theft: Take photos or videos of the damaged or stolen items to provide evidence of their condition. Make a detailed list of the items, including their description, approximate value, and purchase receipts if available. This will help facilitate the claims process and ensure that you receive appropriate compensation.

3. Notify your insurance company: Contact your insurance company as soon as possible to report the damage or theft. Provide them with all the necessary information, including the date and location of the incident, a description of the items involved, and any supporting documentation you have gathered.

4. Cooperate with the claims adjuster: Your insurance company will often assign a claims adjuster to assess the damage and determine the amount of compensation you are eligible to receive. Be cooperative and provide any requested documentation or information promptly to expedite the claims process.

5. Obtain repair estimates or replacement quotes: If your belongings are damaged, gather repair estimates from reputable professionals or vendors. For stolen items, obtain quotes for their replacement cost. Submit these estimates or quotes to your insurance company for review and approval.

6. Follow any additional instructions: Your insurance company may have specific requirements or procedures for filing a claim for stored belongings. It is important to follow any additional instructions they provide to ensure your claim is processed smoothly.

7. Review the settlement offer: Once the claims adjuster has completed their assessment, your insurance company will provide a settlement offer. Review this offer carefully, ensuring that it adequately covers the damage or theft of your stored belongings. If you have any questions or concerns, don’t hesitate to reach out to your insurance company for clarification.

8. Accept or negotiate the settlement: If you are satisfied with the settlement offer, you can accept it and proceed with the settlement process. If you believe the offer is insufficient, you can negotiate with your insurance company by providing additional evidence or documentation to support your claim.

Overview of State Farm’s claims process

State Farm is one example of an insurance company that offers coverage for stored belongings. Here is an overview of the claims process with State Farm:

1. Report the claim: Contact your State Farm agent or the claims department to report the damage or theft of your stored belongings. Provide them with all the necessary information and documentation.

2. Assign a claims representative: State Farm will assign a dedicated claims representative to handle your claim. This representative will guide you through the process and answer any questions you may have.

3. Damage assessment: The claims representative will assess the damage to your stored belongings and determine the cause and extent of the loss. They may request additional documentation or inspections if needed.

4. Claims settlement: After the assessment is complete, State Farm will provide you with a settlement offer. Review the offer carefully and discuss any concerns or questions with your claims representative.

5. Resolution and payment: If you accept the settlement offer, State Farm will work to finalize the claim and issue the payment to you. The timeline for resolution and payment will vary depending on the complexity of the claim.

It is important to note that the claims process may vary depending on your insurance company and policy. It is recommended to review your specific insurance policy and contact your insurance company directly for detailed information on their claims process.

By following the necessary steps and cooperating with your insurance company, you can ensure a smoother and more efficient claims process for your damaged or stolen items in storage.

Tips for Protecting Stored Belongings

Advice on securing and protecting items in a storage unit

When it comes to storing your personal belongings in a storage unit, it’s important to take certain precautions to ensure their safety. Here are some tips to help protect your stored belongings:

1. Choose a reputable storage facility: Select a storage company that has good reviews and a strong security system in place. Look for features like surveillance cameras, gated access, and on-site personnel to enhance the safety of your stored items.

2. Use proper packing materials: Pack your items in sturdy boxes and use packing materials like bubble wrap or packing peanuts to cushion fragile items. This will help prevent damage during transportation and while in storage.

3. Create an inventory: Before storing your belongings, make a detailed inventory of what you are storing. Take photos of valuable items and keep a record of their serial numbers or other identifying information. This can be helpful in the event of loss or damage and when filing an insurance claim.

4. Utilize locks and security devices: Use a high-quality lock to secure your storage unit. Consider using additional security devices such as padlocks or security alarms for added protection. These measures can deter potential thieves and provide an extra layer of security.

5. Avoid storing valuable or irreplaceable items: While renters insurance can provide coverage for your stored belongings, it’s always advisable to avoid storing highly valuable or irreplaceable items. Instead, consider keeping such items in a safe deposit box or secure location closer to home.

6. Regularly inspect and maintain the storage unit: Visit your storage unit periodically to inspect its condition. Look for signs of water leaks or pest infestations, as these can cause damage to your stored items. Report any issues to the storage facility management promptly.

Best practices to prevent damage or theft

In addition to securing your storage unit, there are some best practices you can follow to minimize the risk of damage or theft:

1. Avoid overpacking: Overloading your storage unit can increase the risk of items being damaged or broken. Be mindful of weight restrictions and ensure that items are stacked and stored properly, with heavier items placed at the bottom.

2. Leave space for air circulation: Allow for proper airflow within the storage unit by leaving space between your items and the walls. This can help prevent moisture buildup, which can lead to mold and mildew.

3. Opt for climate-controlled storage: Consider renting a climate-controlled storage unit, especially if you are storing sensitive items like wooden furniture, electronics, or artwork. This can help regulate temperature and humidity levels, protecting your belongings from extreme conditions.

4. Maintain insurance coverage: Keep your renters insurance or storage insurance policy up to date to ensure that your stored items are adequately protected. Review your policy regularly and make any necessary adjustments based on the value and quantity of your stored belongings.

By following these tips and best practices, you can help safeguard your stored belongings and minimize the risk of damage or theft. Remember to read your insurance policy thoroughly and consult with your insurance agent to understand the specific coverage and requirements for storing items in a storage unit. With proper precautions in place, you can have peace of mind knowing that your belongings are protected, even when they are not in your home.

Tips for Protecting Stored Belongings

Advice on securing and protecting items in a storage unit

When it comes to storing your personal belongings in a storage unit, it’s important to take certain precautions to ensure their safety. Here are some tips to help protect your stored belongings:

– Choose a reputable storage facility: Select a storage company that has good reviews and a strong security system in place. Look for features like surveillance cameras, gated access, and on-site personnel to enhance the safety of your stored items.

– Use proper packing materials: Pack your items in sturdy boxes and use packing materials like bubble wrap or packing peanuts to cushion fragile items. This will help prevent damage during transportation and while in storage.

– Create an inventory: Before storing your belongings, make a detailed inventory of what you are storing. Take photos of valuable items and keep a record of their serial numbers or other identifying information. This can be helpful in the event of loss or damage and when filing an insurance claim.

– Utilize locks and security devices: Use a high-quality lock to secure your storage unit. Consider using additional security devices such as padlocks or security alarms for added protection. These measures can deter potential thieves and provide an extra layer of security.

– Avoid storing valuable or irreplaceable items: While renters insurance can provide coverage for your stored belongings, it’s always advisable to avoid storing highly valuable or irreplaceable items. Instead, consider keeping such items in a safe deposit box or secure location closer to home.

– Regularly inspect and maintain the storage unit: Visit your storage unit periodically to inspect its condition. Look for signs of water leaks or pest infestations, as these can cause damage to your stored items. Report any issues to the storage facility management promptly.

Best practices to prevent damage or theft

In addition to securing your storage unit, there are some best practices you can follow to minimize the risk of damage or theft:

– Avoid overpacking: Overloading your storage unit can increase the risk of items being damaged or broken. Be mindful of weight restrictions and ensure that items are stacked and stored properly, with heavier items placed at the bottom.

– Leave space for air circulation: Allow for proper airflow within the storage unit by leaving space between your items and the walls. This can help prevent moisture buildup, which can lead to mold and mildew.

– Opt for climate-controlled storage: Consider renting a climate-controlled storage unit, especially if you are storing sensitive items like wooden furniture, electronics, or artwork. This can help regulate temperature and humidity levels, protecting your belongings from extreme conditions.

– Maintain insurance coverage: Keep your renters insurance or storage insurance policy up to date to ensure that your stored items are adequately protected. Review your policy regularly and make any necessary adjustments based on the value and quantity of your stored belongings.

By following these tips and best practices, you can help safeguard your stored belongings and minimize the risk of damage or theft. Remember to read your insurance policy thoroughly and consult with your insurance agent to understand the specific coverage and requirements for storing items in a storage unit. With proper precautions in place, you can have peace of mind knowing that your belongings are protected, even when they are not in your home.

Conclusion

Storing your personal belongings in a storage unit can provide you with extra space and convenience. However, it’s important to take proper precautions to protect your stored items from damage or theft. Choosing a reputable storage facility, using proper packing materials, and maintaining insurance coverage are all essential steps to ensure the safety of your belongings. By following the tips and best practices outlined in this article, you can have peace of mind knowing that your stored items are protected.

Read more about Storage unit flood insurance.